Poisa Kotha 2: A Series on Financial Literacy

“So, if I can’t become a crorepati by Ponzi schemes, what should I do?”

“My salary isn’t much, so how can I still reach my crorepati goal?”

“I want to retire at 65 with 1 crore or more. How much should I save each month to make this happen?”

Some people dream of becoming a crorepati, while others simply want a steady monthly income for life. Regardless of your goal, there are three important factors that can help you achieve financial success:

- Compounding effect

- Time

- Return on investment

Let’s explore these three factors in detail today. I hope that understanding them will empower you to plan for any financial goal, whether it’s retiring early, buying land, planning for your children’s college education or owning a Jimny the right way!

Compounding Effect:

The compounding effect means your money grows faster over time because you earn interest not just on your original amount (principal) but also on accumulated interest. Picture a minibus rolling downhill from PR Hill to High School junction, picking up more and more passengers as it goes. By the time it reaches the destination, it’s packed with passengers who survived the pothole, bumpy roads. But the only truly happy person during this journey? The conductor! I can’t say the same for the passengers.

In financial terms, if you save Rs. 10,000 at a 4% annual return compounded yearly, here’s how your money will grow:

• Year 1: Interest = Rs. 10,000 × 4% = Rs. 400

Total balance = Rs. 10,400

• Year 2: Interest = Rs. 10,400 × 4% = Rs. 416

Total balance = Rs. 10,816

• Year 3: Interest = Rs. 10,816 × 4% = Rs. 432.64

Total balance = Rs. 11,248.64

You earn interest on both your initial Rs. 10,000 and the accumulated interest from previous years — that’s compounding! You will be a happy conductor at the end of the journey!

If you want to see how compounding works, the easiest way is to punch this prompt into ChatGPT.

“Calculate the compound interest on Rs. 10,000 with an annual interest rate of 4%, compounded yearly, for 3 years. Show the interest earned at the end of each year and the total balance after each year. Explain clearly how the interest is calculated each year, highlighting the compounding effect—how interest is earned not only on the initial amount but also on the interest from previous years.”

Feel free to change the investment amount, rate of return and the year.

And, if you want to use the calculator, there are online calculators such as this fncalculator.com

Time and Rate of Return:

Now that you understand compounding, let’s see why time and returns matter. Unless you win a Rs. 1 crore lottery tonight, your savings need time to compound and grow.

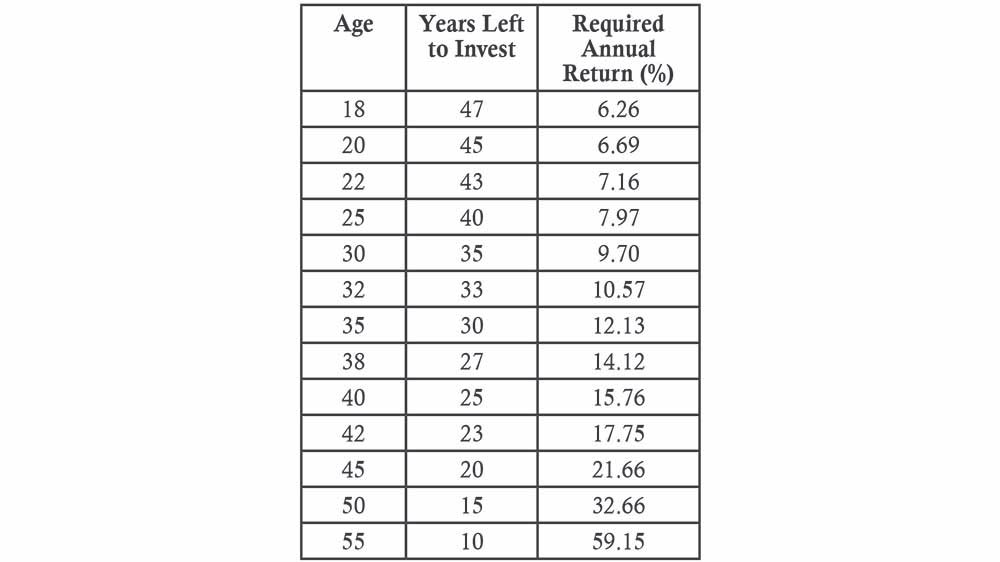

So, how long does it take? Here’s a table showing the required annual returns for different starting ages investing Rs. 3,000 per month to achieve Rs. 1 crore by age 65:

If you start young (18–22), a realistic 6–7% annual return can help you reach a crore! But the closer you get to age 35 or beyond, the higher returns you’ll need — some of which may be too aggressive or unrealistic. In such situations, you will need to invest more than Rs.3,000 per month. I’m just using Rs.3,000 for the sake of this discussion. You can and should always base your savings plan on a monthly budget you can comfortably set aside to achieve your financial goals.

Where to Get These Returns?

To make your money work for you, consider investing in mutual funds through your bank or financial advisor. Walk into your bank and ask them if they can help you invest in mutual funds. Or talk to your qualified financial advisor. Find low-cost funds with good returns tailored to your goals and watch out for fees that can potentially eat into your earnings.

Final Thoughts:

Starting early matters. Even a year of delay can cost you significantly because of missed compounding — that’s the opportunity cost. For those who say “I’ll start later,” remember, time is your most valuable asset!

In my next article, I’ll dive deep into opportunity cost and why time is crucial in wealth-building.

Until then, may the power of compounding be with you as you journey toward your financial goals.

Disclaimer: This guide is provided solely for educational purposes to raise financial awareness and help you make informed decisions. It is not investment advice, nor is it a solicitation or endorsement of any financial products or services. Always consult with certified financial advisors and invest only through well-established and regulated companies to ensure the safety and suitability of your investments.